[et_pb_section admin_label=”section”]

[et_pb_row admin_label=”row”]

[et_pb_column type=”4_4″][et_pb_text admin_label=”Text”]

One way to get your flip project funded quickly is with a hard money loan. We discuss how to use hard money loans to finance house flipping below.

Find a Good Hard Money Lender

Hard Money Lenders Directory

Your first step should be to visit our Hard Money Lenders Directory here. There can find many reputable lenders in all 50 states or by city.

Online Search

You can easily search online for a local hard money lender that will work with new and experienced flippers. We suggest Googling “hard money lenders YOUR CITY NAME”. Local lenders with experience and knowledge of your real estate market are usually the best place to start. If you already have experience rehabbing and flipping properties, you may be able to get more favorable rates than a newbie.

Real Estate Groups

Whether online or in-person, real estate flipping or investment groups can provide you with connections to good hard money lenders. Getting a personal recommendation from another experienced house flipper can save a lot of time and help build a solid relationship from day one.

How to Assess a Hard Money Lender

The best way to assess the professionalism and quality of a hard money lender is to talk to other real estate flippers. However, you can do your own due diligence fairly easily. Speaking to lenders on the phone will allow you to ask questions and see if they are a good fit.

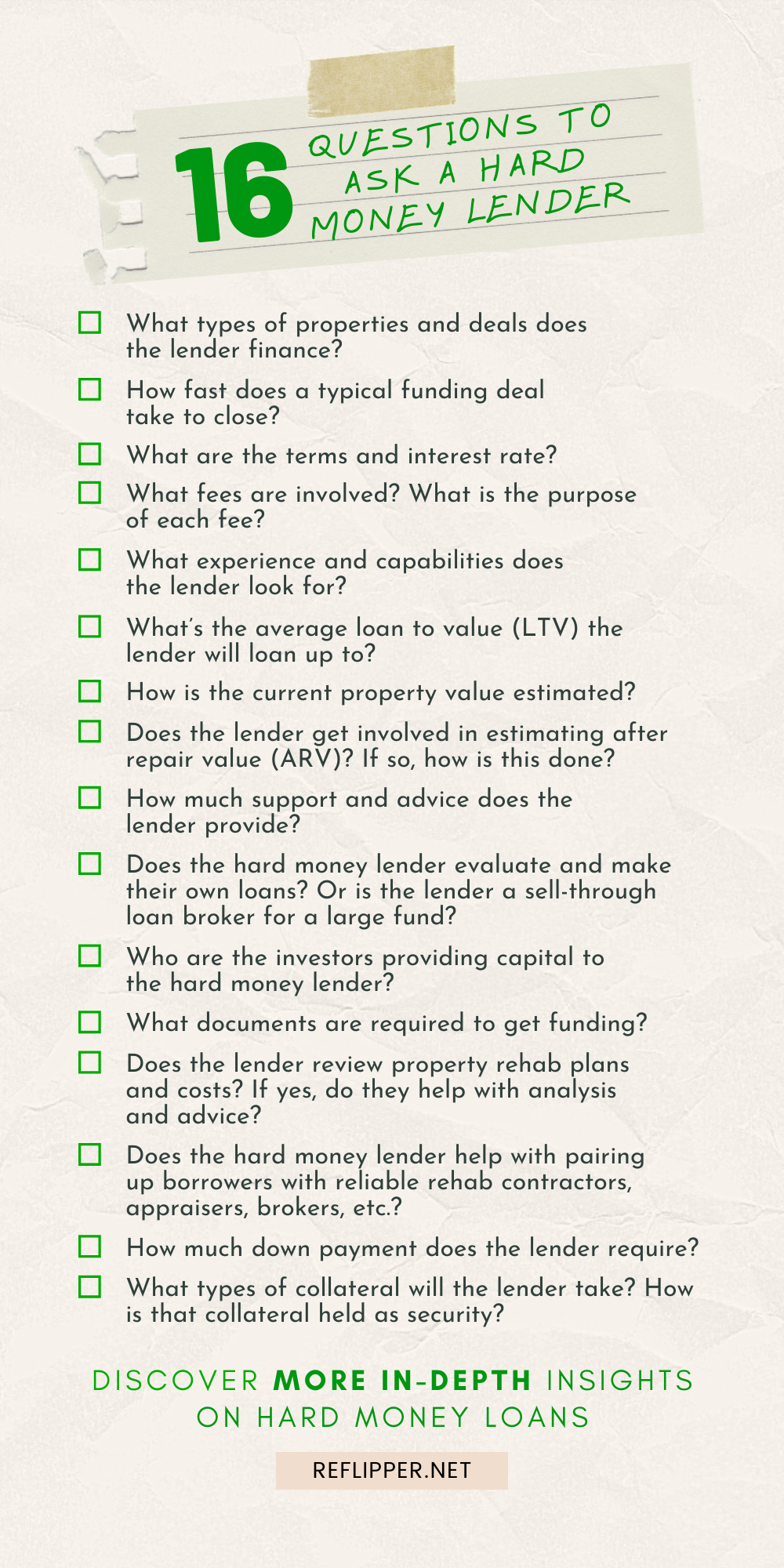

Important questions to ask a hard money lender:

- What types of properties and deals does the lender finance? (e.g. fix & flip, foreclosures, REOs, single family, multi-family, etc.)

- How fast does a typical funding deal take to close?

- What are the terms and interest rate?

- What fees are involved? What is the purpose of each fee?

- What experience and capabilities does the lender look for?

- What’s the average loan to value (LTV) the lender will loan up to?

- How is the current property value estimated?

- Does the lender get involved in estimating after repair value (ARV)? If so, how is this done?

- How much support and advice does the lender provide?

- Does the hard money lender evaluate and make their own loans? Or is the lender a sell-through loan broker for a large fund?

- Who are the investors providing capital to the hard money lender?

- What documents are required to get funding?

- Does the lender review property rehab plans and costs? If yes, do they help with analysis and advice?

- Does the hard money lender help with pairing up borrowers with reliable rehab contractors, appraisers, brokers, etc.

- How much down payment does the lender require?

- What types of collateral will the lender take? How is that collateral held as security?

Hard Money Worst-Case Scenarios

Hard money loans used to fund house flips can go bad for a number of reasons. Preempting these situations with good planning is must.

Funding that was promised may not come through. Your project may get delayed, causing cash flow issues and putting the loan into default. Unexpected fees can show up near the end of the process. An aggressive hard money lender may attempt to foreclose on the property so they can take it.

If contract terms were not clearly defined and understood at the beginning of the process, potential legal battles can ensue.

It is important for borrowers to thoroughly understand the terms of the loan and the hard money lender’s motives. Since most hard money loans are made to companies rather than individuals, you will have minimal legal protection should the deal go bad.

The bottom line is this: Ask lots of questions, understand the moving parts, and pick the right lender before you take out a hard money loan.

Know Your Hard Money Loan Definitions

Knowing all the moving parts before you apply for a loan will put you way ahead. Take some time to review these definitions below. This is important!

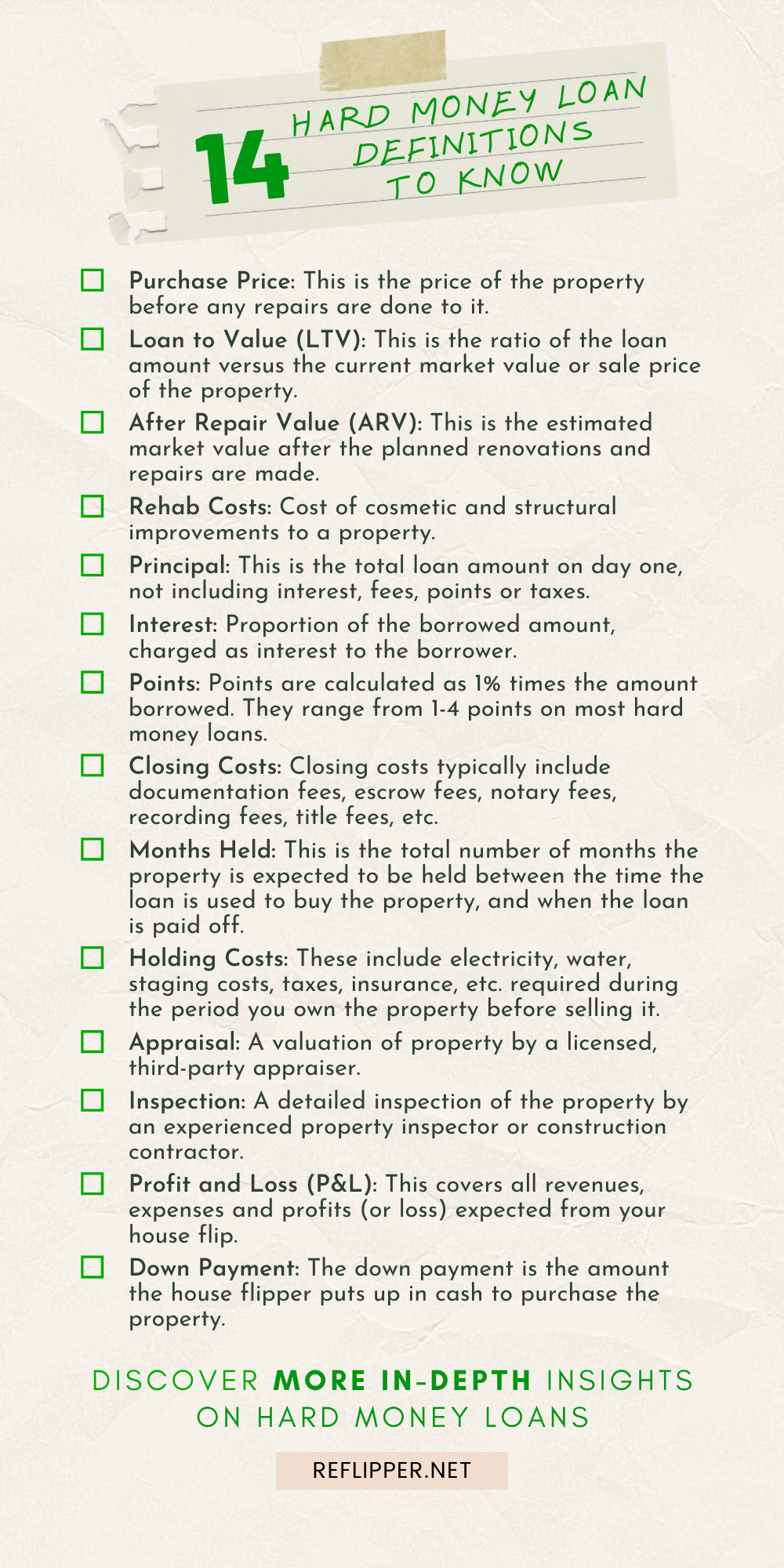

Purchase Price – This is the price of the property before any repairs are done to it. This value is used as the denominator in the Loan to Value (LTV) calculation.

Loan to Value (LTV) – This is the ratio of the loan amount versus the current market value or sale price of the property. Hard money lenders will loan up to a maximum LTV of 65-75%. The rest of the money must be provided by the house flipper or an equity investor.

After Repair Value (ARV) – This is the estimated market value after the planned renovations and repairs are made. ARV is determined by averaging the last three “like” properties in the area that sold in the last six months within a close radius of the property.

Rehab Costs – This is obvious. But communicating these costs to the lender requires a detailed plan of all repairs and renovations expected. This includes all cosmetic and structural improvements. You can get estimates from a contractor. The hard money lender wants to see a realistic budget and plan. They will go over this with you in detail so they understand exactly what you are planning to do on the property.

Principal – This is the total loan amount on day one, not including interest, fees, points or taxes.

Interest – Interest is charged on a monthly basis. Interest payments cannot be missed or your hard money loan will go into default.

Points – Points are calculated as 1% times the amount borrowed. They range from 1-4 points on most hard money loans. These are added to the total repayment amount. Points are charged to offset the up-front research, salary and commission costs incurred by the lender.

Closing Costs – Closing costs typically include documentation fees, escrow fees, notary fees, recording fees, title fees, etc.

Months Held – This is the total number of months the property is expected to be held between the time the loan is used to buy the property, and when the loan is paid off. In a house flip situation, usually the hard money loan is paid off when the house is sold. If the hard money loan is refinanced and paid off that way, then the months held goes up to the date of expected refinancing.

Holding Costs – These include electricity, water, staging costs, taxes, insurance, etc. required during the period you own the property before selling it.

Appraisal – To get a hard money loan to buy a flip house requires an appraisal from a third party. Some lenders only require a “drive-by” appraisal with detailed photos and items that need to be repaired.

Inspection – A detailed inspection of the property by an experienced property inspector or construction contractor is essential. This highlights any major cost issues, such as termites or rot, HVAC, roof, or plumbing problems. If major repairs or reconstruction are needed, the city may require one of their inspectors to visit and sign off, as well. This is necessary if permits are required to meet local building codes.

Profit and Loss (P&L) – This covers all revenues, expenses and profits (or loss) expected from your house flip. Since it’s forward-looking (aka “pro forma”) the Profit and Loss statement is just an estimate. See below for how to calculate P&L.

Down Payment – The down payment is the amount the house flipper puts up in cash to purchase the property. A sufficient down payment is mandatory to secure a hard money loan. You transfer the funds seller on closing the property purchase. The money can come from anywhere. The hard money lender just wants to see the proof of funds, not where you get it from. Funds can come from friends, bank loans, family, your savings, etc.

Choose the Right House to Flip

When buying and flipping houses using hard money loans, it’s essential to choose the right house.

Hard money loans are not ideal for long term financing because they charge high interest rates. So you should think about buying properties that can be either flipped immediately, or require mostly cosmetic repairs for a fix & flip.

You can still use hard money loans to rehab properties with significant structural issues. If that’s the case, you should a) have solid experience and a team to do complex and expensive renovation work, and b) buy properties at a very significant discount to the future ARV. For example, you can use hard money loans to buy and rehab beat up houses at foreclosure auctions.

If you choose a house that needs significant cosmetic and structural repairs then pick the most run-down house on the block in a good area. This lets you quickly “upscale” the house to match the surrounding comps. These deals don’t come very often, but are more available in market downturns.

If you’re new to the fix & flip business, a hard money lender may reject you for a property that is too damaged. Judgement is needed here before you pick a property and apply for a loan.

Calculating the Profit of a House Flip Financed with Hard Money

You can use this basic formula below to estimate the P&L of a house flip using a hard money loan.

REVENUE (the estimated ARV of the property when you sell it)

minus

PURCHASE PRICE (before rehab)

minus

REHAB COSTS

Buying and Selling Costs

- Purchase closing costs

- Broker purchase commission (if you use one)

- Marketing costs

- Broker sale commission (if you use one)

Rehab Costs

- Cleanup

- Interior paint

- Refinish floors and railings

- Replace trim, screens, outlet and switch covers

- Replace appliances

- Replace cabinets and counter tops (where applicable)

- Fixtures (lights mostly)

- Roof

- Exterior Paint

- Landscaping

- Miscellaneous (add 10-20% buffer)

Carrying Costs

- Insurance

- Property taxes

- Maintenance

- Utilities

- Security (to prevent vandalism and theft during rehab)

Financing Costs

- Doc fees

- Processing fee

- Appraisal fee

- Inspection fee

- Total interest (paid monthly interest)

- Points

= TOTAL PROFIT (or loss)

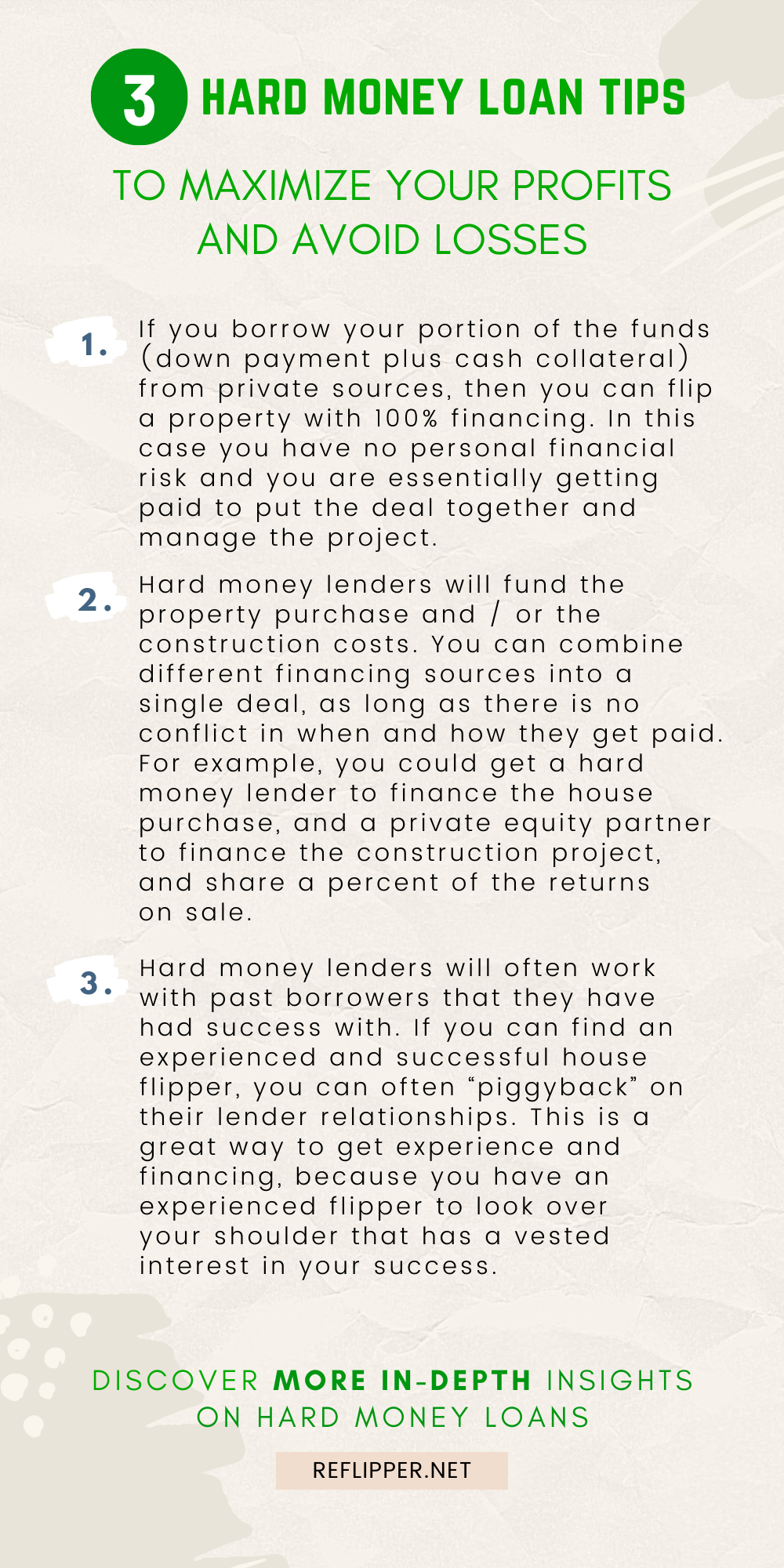

Tips to Maximize Your Profits (and Avoid Losses)

TIP #1: If you borrow your portion of the funds (down payment plus cash collateral) from private sources, then you can flip a property with 100% financing. In this case you have no personal financial risk and you are essentially getting paid to put the deal together and manage the project.

TIP #2: Hard money lenders will fund the property purchase and / or the construction costs. You can combine different financing sources into a single deal, as long as there is no conflict in when and how they get paid. For example, you could get a hard money lender to finance the house purchase, and a private equity partner to finance the construction project, and share a percent of the returns on sale.

TIP #3: Hard money lenders will often work with past borrowers that they have had success with. if you can find an experienced and successful house flipper to work with, you can often “piggyback” on their lender relationships. This is a great way to get experience and financing, because you have an experienced flipper to look over your shoulder that has a vested interest in your success.

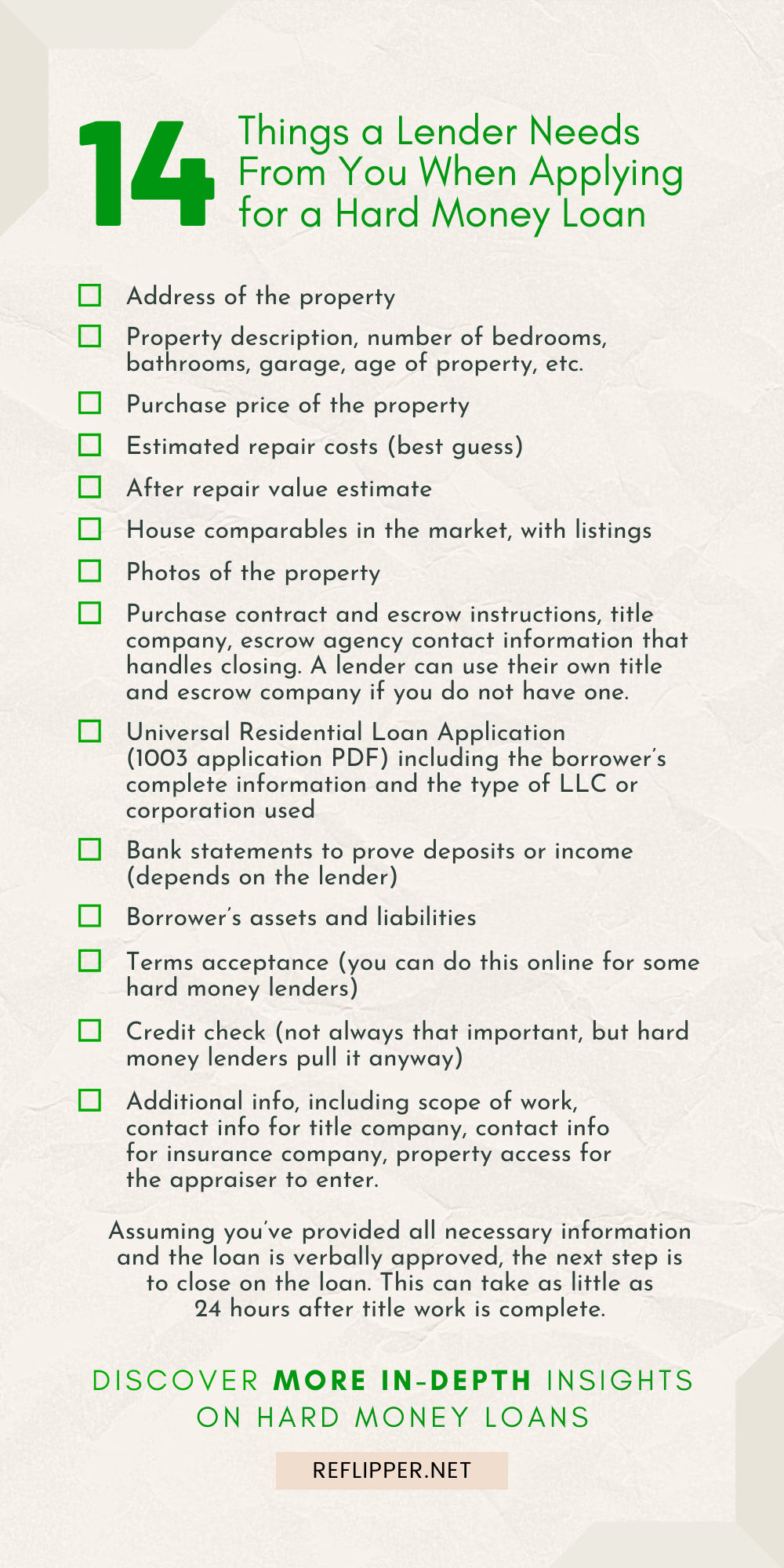

What a Lender Needs From You When Applying for a Hard Money Loan

Before applying for a hard money loan, you will need to get all your ducks in a row. Here’s what you’ll need:

1. Address of the property

2. Property description, number of bedrooms, bathrooms, garage, age of property, etc.

3. Purchase price of the property

4. Estimated repair costs (best guess)

5. After repair value estimate

6. House comparables in the market, with listings

7. Photos of the property

8. Purchase contract and Escrow instructions, title company, escrow agency contact information that handles closing. A lender can use their own title and escrow company if you do not have one.

9. Universal Residential Loan Application (1003 application PDF) including the borrower’s complete information, and the type of LLC or corporation used

10. Bank statements to prove deposits, or income (depends on the lender)

11. Borrower’s assets and liabilities

12. Terms acceptance (you can do this online for some hard money lenders)

13. Credit check (not always that important, but hard money lenders pull it anyway)

14. Additional info, including scope of work, contact info for title company, contact info for insurance company, property access for the appraiser to enter.

Assuming you’ve provided all necessary information and the loan is verbally approved, the next step is to close on the loan. This can take as little as 24 hours after title work is complete.

Wisdom From the Trenches – Using Hard Money Loans for House Flipping

Hard Money Lenders Move Fast

Most of the steps above happen within 24 hours because hard money lenders move fast. You can even get a quote over the phone. The lender will use the MLS at their office to search the property and neighborhood.

Hard money lenders want to fund your deal quickly so they don’t lose it. So they act quickly to get the fix and flip process moving forward.

Risk Level of the Property Matters Most

Qualifying for a hard money loan – and the interest rate you pay – depends mostly on the risk level of the property. Banks will not take the risk on a property that needs lots of repairs. This is why hard money lenders charge much higher rates. The higher the risk to the lender, the higher the rates and down payment will be.

The best advice is this: If you’re relatively new to house flipping, or the your market is not moving up strongly, then pick a simple flip property with minimum construction issues to finance with hard money. Your costs will be much lower because the risk to the lender will be much lower.

What to Be 100% Sure Of

Don’t overestimate the value of the property (either current value or ARV).

Overestimate your rehab costs. Build a buffer of 10-20% into your cost projections.

Ask lots of questions of the lender (see above). Know every detail!

Be as precise with your numbers. Reference recent market values and get quotes from credible contractors whenever possible. A few percentage points off, and you can end up owing a lot more money!

Use Local Hard Money Lenders

You should always start with a local hard money lender (see our Hard Money Lenders Directory to find one in your area). You want to work with an expert in your geographical area because they bring a wealth of connections and advice to succeed. Go to meetups to find them or ask for referrals from other flippers.

Beware of Sharky Lenders

A good hard money lender will be structured, competent, and complete the process within a few days, not weeks. They also will be able to arrange their own appraisals and inspections, and have a network of service providers to help them.

Using a bad hard money lender can ruin your house flip deal, and potentially your credit. An inexperienced or untrustworthy hard money lender may skip steps, or add on a litany of unexplained fees. If you sense this is happening, then move onto another lender. It’s best to be cautious in this regard.

Many things can go wrong during a fix and flip later on in the process, so getting started on the wrong foot with a sharky hard money lender is bad news. If you get stuck in a bad hard money loan, you can quickly end up in a foreclosure or worse.

Don’t Give Up

New hard money borrowers need to be confident in their abilities to negotiate. You should not give up if the first deal does not work out. Keep discussing your issues with fellow flippers and real estate investors to find a hard money lender you can work with. Never accept a bad deal just because you fear that you won’t be able to get financing.

To Recap…

A hard money loan can allow you to finance a house flip fast so you can rehab and sell it for a profit quickly. Being prepared for the process of getting a hard money loan will keep your house flip project on time while protecting you from any unnecessary risks. Following these guidelines to use hard money loans to finance house flipping will help your business profit.

[/et_pb_text][/et_pb_column]

[/et_pb_row]

[/et_pb_section]